Two Markets, One Reset: A Healthier Model for Startup Funding

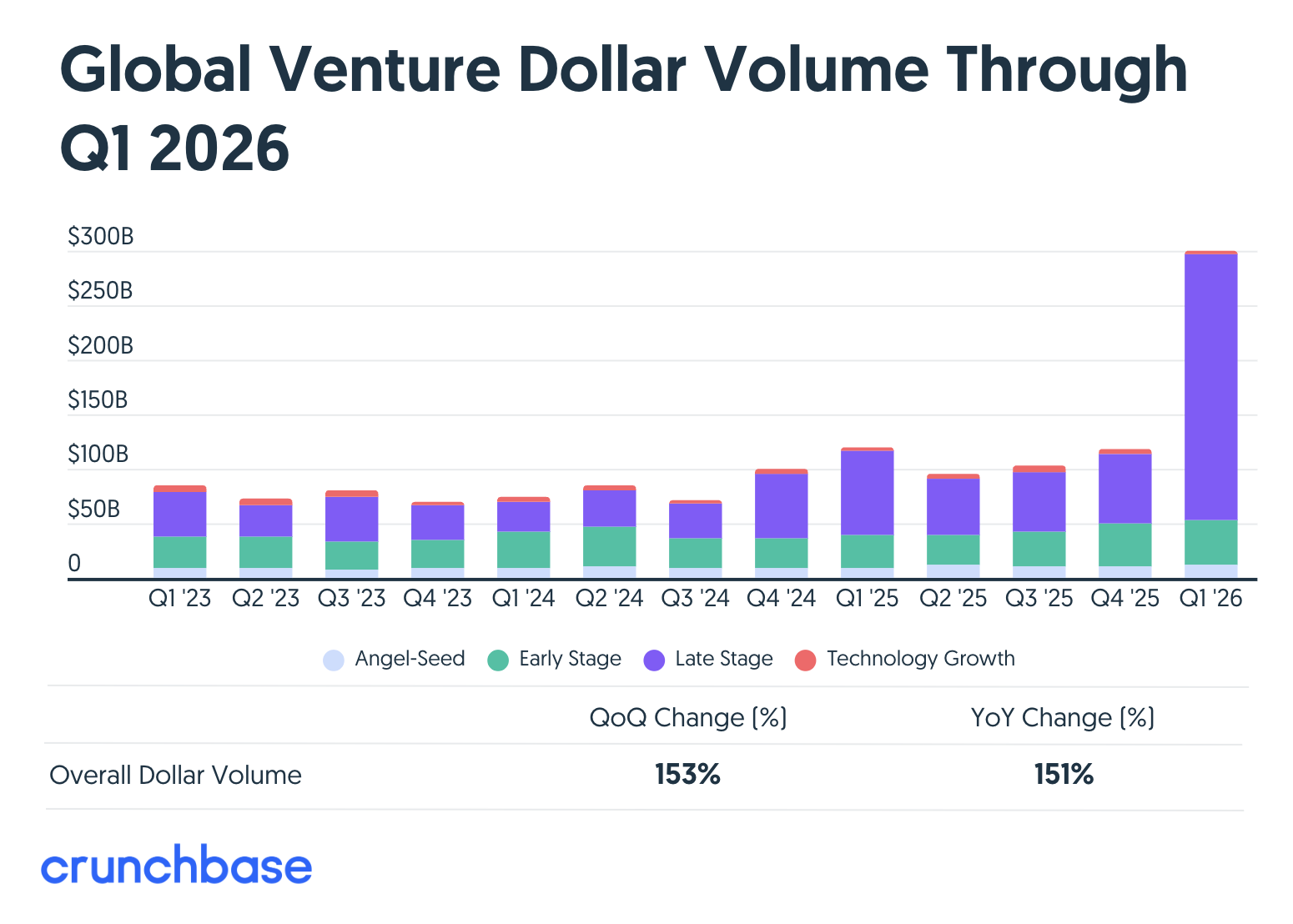

In the first quarter of 2026, investors poured roughly $297 billion into about 6,000 startups globally — up around 150% quarter over quarter and year over year. That single quarter accounted for nearly 70% of all venture capital spending in 2025, and topped every full-year total before 2018.

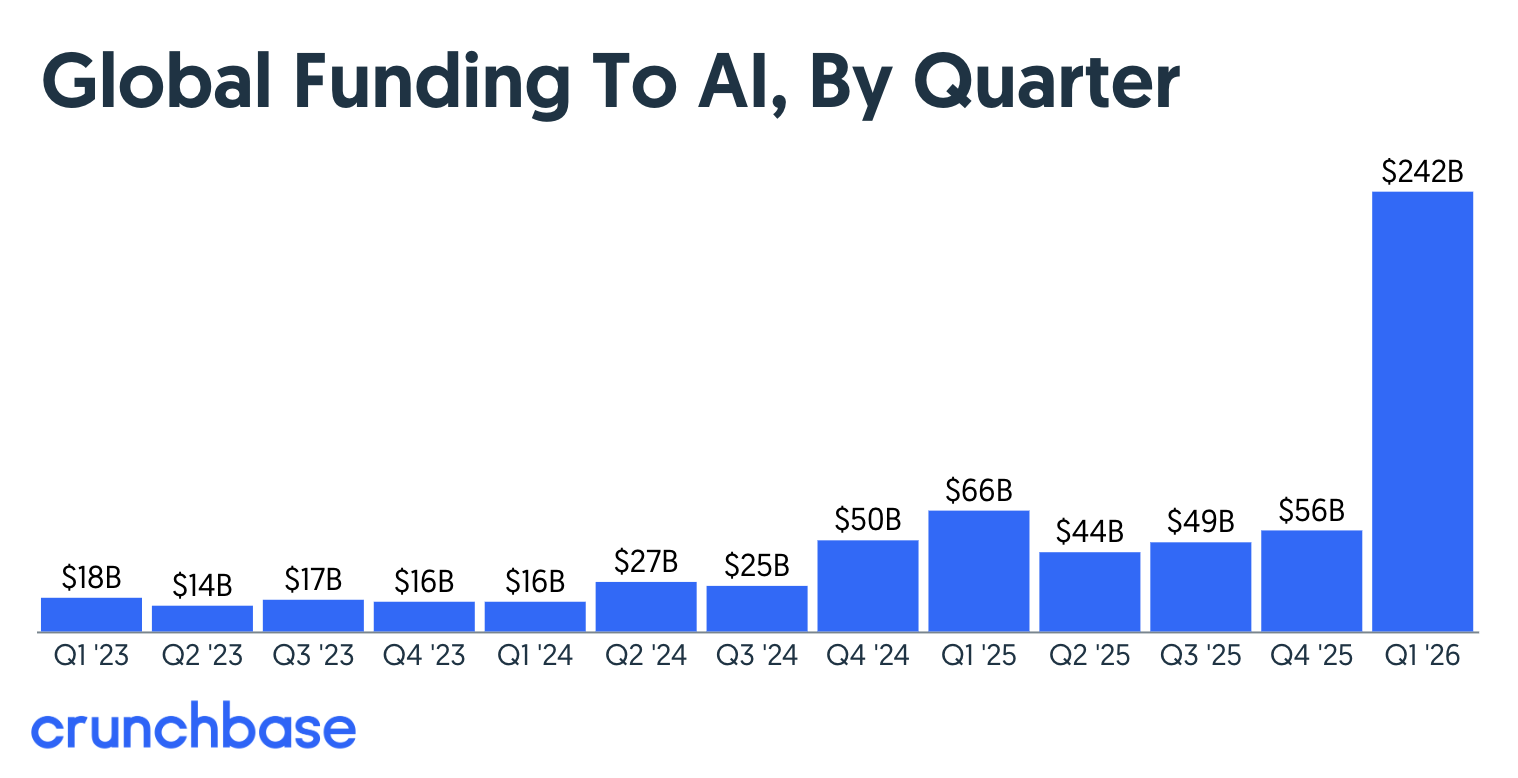

By any conventional reading, venture capital is back, and bigger than it has ever been. But the headlines obscure another story. Of that $297 billion, $239 billion — 81% of total global venture funding — went to AI. Just four companies — OpenAI, Anthropic, xAI, and Waymo — collectively raised $186 billion, or 64% of global venture investment in the quarter.

Four of the five largest venture rounds ever recorded closed in Q1 2026. And U.S.-based companies captured 83% of global venture capital, with the BayArea absorbing the lion's share of the AI flows. Step back to the full year prior, and the same pattern shows up at the macro level. Of roughly $425 billion deployed globally in 2025, $211 billion — nearly half — went to AI, and five companies alone captured $84 billion, or 20% of all global venture capital deployed that year.

Megarounds of $500 million and more captured a third of all global funding. Seed deal counts, meanwhile, kept declining. As PitchBook puts it, the gap between the haves and have-nots has expanded sharply.

So what is actually happening? Two things at once, and they cut in opposite directions.

For a tiny number of frontier AI companies and the firms close enough to write nine- and ten-figure checks into them, this is the most concentrated capital event in the history of private markets. For everyone else — every founder outside that vortex, every fund without a position in it, every employee at a non-AI company looking at the cap table they signed in 2021 — the contraction that began in 2022 has continued, deepened, and started to reshape the industry in ways most participants haven't yet absorbed.

This blog is about the second story, because that's the one that matters for the next decade of company-building.

Five Realities for Founders

Before the structural analysis, it helps to name what this actually feels like on the ground for founders trying to build outside the AI megaround economy. Five realities are reshaping how good companies get started, funded, and scaled right now:

Small and medium-sized VCs have a harder time raising, and have less to deploy. LP capital is flowing toward whichever firms can credibly claim a position in the frontier AI rounds, which means sub-scale and middle-market funds are getting starved. Many won't raise their next vehicle. Many that did raise are deploying more cautiously than their fund size implies, holding reserves for follow-ons in a market where exits remain elusive. The practical implication for founders is that the long tail of investors who used to lead Series A and Series B rounds is thinning out — and the firm that wrote your seed check may not be the firm that exists when you need a bridge.

Startups have to compete harder, for less favorable term sheets. With fewer firms actively writing checks and more high-quality companies competing for each of those checks, negotiating leverage has shifted toward investors. Founders who would have run a competitive process two years ago are increasingly taking the first viable term sheet they get. That means longer diligence cycles, slower decisions, more structure in the term sheet — milestone tranches, expanded pro rata rights, observer seats, side letters — and lower entry valuations relative to actual traction. The headline number on a deal matters less than ever; the terms behind it matter more.

Higher entropy in the market makes it harder to identify the right problem to solve. AI is collapsing the cost of producing software and shifting what's actually defensible at the same time. Categories that looked like obvious investments two years ago — vertical SaaS, applications layers, point solutions — are suddenly susceptible to being subsumed by a foundation model with a workflow wrapper. Categories that looked like science projects are now fundable in a single weekend. The signal-to-noise ratio has gotten worse, not better, and the work of figuring out which problem is worth a decade of a founder's life is harder than it has been in any cycle in memory.

Higher velocity means shorter build cycles and thinner moats to defend. When a competent team can ship a credible v1 in six weeks using AI tooling, the window between launch and competitive parity is collapsing. Pure software differentiation, which carried so many companies through the last cycle, increasingly isn't enough. Durable moats now look more like distribution, proprietary data, regulatory positioning, hardware, and deep customer relationships — the things AI cannot replicate from a prompt. Founders who don't actively build for one of those moats from day one will find themselves running a feature, not a company.

Founders should raise capital when they are truly ready to grow — not before. Raising prematurely was the cardinal sin of the last cycle. Doing it in this environment is worse, because the cost of capital is higher, the dilution is steeper, and the structure that comes attached is stickier and harder to unwind. The right time to raise is when there is a specific, identifiable use of capital that produces a step-change in the business — a hire, a market entry, a product line, a contract that requires inventory. Not when capital is "available." Not when a deck happens to be ready. Not because peers are raising. Capital taken before a company is ready to deploy it productively becomes its own form of debt — measured not in interest payments but in dilution, distortion, and the obligation to perform a growth story the underlying business can't yet support.

These five realities don't show up on the funding-volume charts. But they're the texture of the market every non-frontier founder is operating inside, and they explain why the macro numbers feel so disconnected from the actual experience of trying to build a company today.

The Diagnosis

Strip out the AI numbers and the picture that remains is bracing. The post-COVID period has produced the most precipitous decline in VC activity, investments, valuations, and exits of the 21st century. The late-2021 peaks were stratospheric, the fall from there has been correspondingly steep, and the right word for what followed in most sectors is nuclear winter. The IPO window stayed shut for years. M&A slowed. Mark-to-market valuations on cap tables stopped meaning much of anything. And while AI numbers were detonating in the foreground, the firms that drove the last cycle quietly started disappearing in the background.

The structural cause is mathematical. In 2010 there were just under 1,000 independent U.S. venture firms. Today there are over 4,000. There are probably more good ideas worth funding now than fifteen years ago, but not nearly enough good ideas to absorb a fourfold expansion in firm count. Capital chased deals that shouldn't have been deals, valuations chased capital, and the gap between paper marks and real outcomes widened until something had to give. The AI concentration of 2025–2026 is, in part, what gives. Capital is consolidating into a tiny set of perceived winners precisely because the rest of the venture economy has gotten harder to underwrite.

The Zombie Phase

Here's the part most founders miss. Venture funds are ten-year vehicles. So when a VC firm dies, it doesn't die quickly — it enters an extended zombie phase where it technically still exists, still holds positions, still appears on cap tables, but no longer raises new funds and can no longer meaningfully support its portfolio companies. The contraction is happening, but it is invisible because the corpses are still standing.

PitchBook counted 574 U.S. zombie VC firms at the start of 2025, up from 382 at the end of 2021. The number of unique investors participating in U.S. venture deals fell roughly 25 percent in a single year — from 15,303 in 2023 to 11,425 in 2024 — the lowest figure in a decade. Distribution rates from older funds have rarely cracked 50 percent over the past ten years, leaving record amounts of NAV trapped in vehicles that should have wound down. MSCI's data shows the median venture fund hitting "zombie age" with nearly 30 percent of committed capital still parked in unrealized positions.

For founders, this matters enormously. If one of your existing investors is a zombie, they may sit on your cap table without participating in your next round, without making intros, without offering meaningful guidance, and without ever signaling whether they intend to support you or quietly run out the clock on their fund. The board seat is still there. The pro rata rights are still there. The judgment and capital are gone.

The Damage Done in the Boom

The zombie problem is the cleanup. The deeper question is what got built during the boom that's now being unwound — and what's being rebuilt the same way inside the AI bubble in real time. The honest answer is that the venture industry, by structurally favoring momentum over durability, did real disservice to entrepreneurs. The dominant playbook of the last cycle pushed CEOs to grow at unsustainable rates so that successive rounds could be raised at ever-higher valuations. Each round looked like a win — a bigger headline number, a fresh injection of capital, a new logo on the deck — but every round also diluted employees, distorted strategy toward whatever metric the next investor wanted to see, and stacked liquidation preferences against founders.

The cumulative effect is brutal. Liquidation preferences are sticky and additive: each new round expects the same protections as the last, and later-stage investors typically demand to be paid out first. Founders who raised aggressively at peak valuations now find themselves running companies where the entire stack of preferred capital exceeds plausible exit prices — meaning their common stock, and their employees' common stock, is functionally worth zero unless the company achieves an outcome dramatically larger than what the business actually supports. That's not a partnership. That's an option that's already been exercised against them.

The good news is that on paper, the worst term-sheet behaviors have receded. Cooley's data shows that 98 percent of Q2 2025 U.S. venture rounds reverted to a 1x non-participating liquidation preference, with cumulative dividends present in only 2.5 percent of deals — the lowest level on record. The bad news is that founders who raised in 2020 and 2021 are still living inside the structures they signed then, and a new generation of complex instruments is rising to take their place. Tranched financings — where capital is committed but only released against milestones — accelerated through the back half of 2025. Used well, they discipline both sides. Used badly, they hand investors a kill switch and force founders to manage to artificial gates rather than to the business. And inside the AI megaround economy, the same growth-at-all-costs dynamics that produced the last cycle's casualties are being repeated at higher valuations, with longer time-to-exit, and with concentration risks that have never existed before in private markets.

The Right-Sizing Is Healthy

The most important thing to understand about the current contraction is that it is not just inevitable but desirable. There are too many sub-scale, undifferentiated firms competing to deploy capital they shouldn't have raised in the first place. Consolidation will produce a healthier industry. Fewer firms, with more conviction, more specialization, more differentiation, and more skin in their portfolio companies' actual outcomes, is what a functional venture market looks like. This is what makes the present moment a real opening. The cycle of growth-at-all-costs broke. The IPO window stayed shut long enough to expose the difference between paper unicorns and real businesses — and notably, despite the record Q1 2026 funding numbers, the IPO market did not reopen in step. AI is absorbing the overwhelming majority of venture dollars, and an unprecedented share of total deal value is going to a vanishingly small fraction of deals — meaning every founder outside the AI gold rush is being forced, whether they want to be or not, into a more disciplined posture. The market is telling everyone the same thing: prove the unit economics, show the trajectory, run the company like it might need to support itself.

What a Healthy Approach Could Look Like

So what should the next generation of startup funding actually look like? A few principles, drawn from what's failing and what's working:

Capital should match the problem, not the cycle. A pre-seed company building a wedge feature does not need a $20M seed round at a $100M post-money. It needs enough money to figure out whether the thing works. The right question is no longer "how much can we raise?" but "how much can we deploy responsibly against the next clear milestone?" Eighteen to twenty-four months of focused runway, sized to a real plan, is almost always healthier than a war chest that tempts the team into premature scaling. This is true at $5 million and it is true at $5 billion.

Growth should be a result, not a target. The most damaging legacy of the last cycle was treating growth rate as the metric that mattered, with everything else — gross margin, retention, payback period, cash efficiency — as secondary. That order needs to be reversed. Growth is what falls out of a business with strong unit economics and real demand. When growth is engineered ahead of those things, you get a company that requires perpetual capital infusions to keep looking like it's working, and a cap table that eventually crushes everyone who isn't a late-stage preferred holder.

Term sheets should be aligned, not adversarial. The market standard of 1x non participating preferred with broad-based weighted-average anti-dilution is a reasonable equilibrium, and founders should fight to keep it. Watch for the silent killers: cumulative dividends that compound during the long private hold, full-ratchet anti-dilution, multiple liquidation preferences that quietly stack across rounds, expansive protective provisions that hand small investors veto rights over operating decisions. The term sheet is not paperwork. It is the constitution of the partnership, and the partnership has to survive both good and bad outcomes.

The investor matters more than the valuation. A $5M round from a firm that will still be raising and supporting in five years is worth more than an $8M round from a firm one bad fund away from zombie status. Founders should diligence their investors as hard as their investors diligence them — fund vintage, fund size relative to deployed capital, recent investment cadence, recent exits, and whether the partner sponsoring the deal has support inside the partnership. If the firm hasn't made a new investment in a year, that's a flag, not a coincidence.

Capital should be fit-for-purpose, not one-size-VC. Venture capital is the right instrument for a specific kind of company — high uncertainty, high upside, where speed and scale create defensibility. It is the wrong instrument for steady cash-flow businesses, capital-light services companies, and product-led businesses that can fund growth out of revenue. Revenue-based financing, strategic corporate capital, non-dilutive grants, secondary liquidity programs, and patient debt all have legitimate roles in a founder's stack. Picking the right form of capital for the stage is more important than picking the most prestigious investor at the highest valuation. And in an environment where corporate balance sheets and PE firms — not traditional VCs — are increasingly leading the largest rounds, founders need to understand who they're actually partnering with and what that partner needs.

Liquidity should be designed in, not waited for. The ten-year fund structure is part of why the zombie phase exists, and it's part of why so much value gets trapped. Secondary markets are projected to exceed $210 billion by early 2026, and structured tenders are becoming a normal part of late-stage company life. Founders should plan for partial liquidity events — for themselves, their early employees, and their early investors — long before an IPO that may or may not happen. Money that comes out of the cap table at a sensible price is money that doesn't have to be conjured by a stretch valuation in the next round.

Boards should govern, not perform. A healthy board is small, balanced between founders and investors, anchored by at least one genuinely independent director, and oriented toward operating reality rather than narrative management. Observer seats should be information-only. Veto rights should be narrow and tied to genuinely existential decisions. The job of a board is to help the company make better decisions and to hold the CEO accountable to outcomes — not to impose the strategic preferences of whichever investor talks loudest in the room.

Where This Lands

The right-sizing of venture capital is going to be uncomfortable for a lot of firms and disorienting for a lot of founders. Many of the cap tables built during the boom are not going to recover. Many of the funds that wrote those checks are not going to raise their next vehicle. Many of the assumptions about what a "successful" startup journey looks like are going to need to be unlearned. And the headline AI numbers — as eye-popping as $297 billion in a single quarter sounds — should not be mistaken for a healthy venture market. They describe an industry in which a small number of frontier bets have absorbed nearly all the oxygen, while the broader system that funds the rest of innovation continues to contract beneath the surface.

Both things are true at once. Pretending otherwise is how founders end up signing the wrong term sheet, with the wrong investor, on the wrong assumptions about what comes next.

The industry that emerges on the other side of this reset will be smaller, more disciplined, more honest about what venture capital is actually for, and better aligned with the founders it backs. The boom rewarded performance.

The reset will reward substance. For founders building real companies, that's the version of the venture market worth wanting.